Investing during inflation

How to help protect your portfolio from high inflation.

Article published: December 22, 2023

Contrary to popular belief, inflation is a normal part of a functioning economy – it can even signify healthy growth. Ordinarily, the decline in purchasing power from rising consumer prices remains relatively modest, allowing consumers to borrow and spend money more freely. But when inflation suddenly spikes, it can become painful for everyone.

For consumers, rising prices may mean spending less as their income is stretched thinner and their savings account loses purchasing power. At the same time, high inflationary times can quickly erode an investment portfolio’s purchasing power as well. So, how do you invest to protect against inflation?

To help you develop a solid investment strategy that acts as an inflation hedge, let’s take a closer look at what high inflation is, how it impacts your portfolio and the best investments to consider for helping you build, grow, protect and preserve your wealth, even in inflationary times.

Understanding high inflation

People often associate higher inflation with higher prices, but at its core, inflation is a decrease in purchasing power when demand outweighs available supply at the average market prices. While it’s easing, the inflation we’re seeing now was caused by three factors coming together: volatility of energy prices, backlogs of work orders for goods and services caused by supply chain issues related to the pandemic, and price changes in the auto-related industries.1

But how does all this drive inflation? Another way to understand what drives inflation is to recognize two primary mechanisms: demand-pull and cost-push.

In the demand-pull effect, an increased money supply leads to a rise in the demand for goods and services. With demand higher than supply, the economy’s production capacity can’t keep up, resulting in an increase in prices.

On the other hand, cost-push inflation is when the cost of production increases due to factors like supply chain disruptions or rising material and labor costs. This causes a decrease in the aggregate supply of goods and services, leading to higher prices.

The government is responsible for keeping the inflation rate in check. This often occurs in three ways, with the first being the most common method, led by the Federal Reserve:

- Raising interest rates to slow the economy by making credit more expensive

- Countering cost-push inflation with supply-side policies to increase aggregate supply

- Countering demand-pull inflation with fiscal policies to decrease demand

Is inflation always bad?

While higher inflation rates can be harmful in the short term, many economists believe that a steady, modest rise in prices is a necessary part of economic growth.2 This is why the Federal Reserve targets a low inflation rate of 2%, based on the Personal Consumption Expenditures price index.3 Of course, the actual rate fluctuates year over year and even month to month. In reality, the average inflation rate between 1960 and 2022 was 3.8%.4

Current inflationary trends

In the last few years, the inflation rate has made numerous headlines, peaking at over 9% in June of 2022 – the highest 12-month rate since 1981.5 Since then, it has continued to fall, landing at 3.1% in November 2023.6 But what caused inflation to spike, and what’s currently driving it?

The pandemic is an obvious answer, and while it did cause significant disruptions, the economy seemed to be leveling out as supply chain issues eased. Then, the major conflict between Russia and Ukraine broke out, impacting essential commodities, like grain and oil. Between the limited supply of goods and services and the increasing production costs, this confluence of events created the perfect storm of both demand-pull and cost-push effects – driving inflation to levels we haven’t seen in several decades.

What does this mean for investors?

Inflation’s impacts on the economy, stock market and individual assets can be unpredictable. That’s why it’s crucial to keep a close eye on your investment portfolio.

While stocks are generally better positioned to help keep pace with inflation than other asset classes, they’re not always able to offset rapidly decreasing purchasing power. However, higher inflation can also harm fixed-rate debt securities, like certain bonds, as it devalues the interest rate payments. This can cause bondholders to actually lose money after adjusting for inflation.

So, what can investors do to implement inflation protection in their portfolios?

Is there a “best way” to protect against inflation?

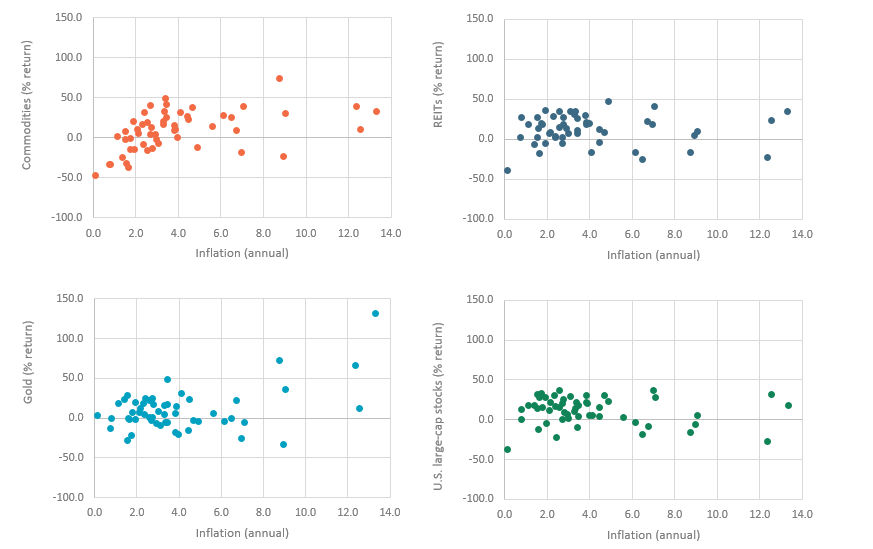

Whenever inflation is a concern, you’ll start hearing more frequent sales pitches for so-called “inflation hedges,” such as gold, commodities or real estate. Do these popular hedges actually work? Let’s look at the historical data. The charts below show how inflation is related to the price of gold, a basket of commodities, and index performance of real estate investment trusts as well as U.S. large-cap stocks every year since 1972.

Source: Ibbotson SBBI, Morningstar Direct; representative indexes for each asset class covering the period from 1970 through June 30, 2023. Representative indexes for each asset class are as follows: Gold (LBMA Gold Price PM USD), Commodities (S&P GSCI TR USD), REITs (FTSE NAREIT All Equity TR USD), U.S. large-cap stocks (IA SBBI US Large Stock TR), Inflation (IA SBBI US Inflation).

As you can see, there’s basically no systematic relationship between the annual returns of these assets and inflation. The relationship between inflation and popular hedges doesn’t appear to be materially different than that of stocks to inflation (while longer-term, stocks have outpaced both gold and commodities).

In the gold chart, you might see a positive (upward-sloping) trend, but that’s driven by a few exceptional years in the upper right. There is a hint of a correlation between commodity prices and inflation. But that positive slope only shows up for years with moderate inflation. And that’s mostly because there’s a mechanical relationship from oil prices being a big component of the CPI basket. But on the right side of that chart, whenever inflation has been higher than 4%, commodities have not provided protection against inflation (and, in fact, they’ve sometimes declined significantly during inflationary periods).

What the data means

There are two lessons you should take away from our brief look at the data:

- None of these assets have proven to be a solid short-term hedge against inflation

- They are all risky assets that should be held only as portions of a diversified portfolio

We wouldn’t recommend overconcentrating in any of these asset classes, even if you’re willing to bet they might be good inflation hedges in the future.

One potential inflation hedge

There actually is an asset that does provide one-for-one inflation protection: Treasury Inflation-Protected Securities. They are guaranteed by the U.S. government to provide returns that are indexed to inflation. You can either buy them directly from the U.S. Treasury, or through mutual funds and ETFs that hold them. TIPS funds are some of the investment options that we consider for portfolios as appropriate. They may be desirable investments to hold to ease inflation and help mitigate risk but only as part of a broadly diversified portfolio.

Investing during inflation – the pros and cons

Staying invested all the time – including during periods of high inflation – enables you to help preserve your portfolio’s worth and maintain your purchasing power. By investing in inflation-protected assets, you can also diversify your holdings to help reduce your overall risk exposure.

On the other hand, changing your investment portfolio during high inflation can expose you to increased risk, potentially weighing certain asset classes too heavily. The goal is to spread the risk across your portfolio with a variety of different holdings. As such, we do not recommend changing your investment strategy during inflationary periods.

For most long-term financial goals, you don’t need to protect your entire nest egg from month-to-month or year-to-year inflation. You should focus on investing your portfolio over the long run. Although there are no guarantees, with a well-diversified portfolio of bonds and stocks, you may be able to achieve returns that can exceed inflation over time.

Fight rising inflation with a financial advisor

As with every investing strategy, there are no guarantees. The best way to hedge against inflation – including what may come in the future – is to speak with your financial planner and ask for professional investment advice.

Looking for a financial advisor who can help you fight high inflation? Reach out to one of our experienced advisors today.

1 U.S. Bureau of Labor Statistics. (2023, January). What caused inflation to spike after 2020? Retrieved December 12, 2023, from

2 International Monetary Fund. (2023). Inflation: Prices on the rise. Retrieved December 12, 2023, from

3 Federal Reserve Board. (2020, August 27). Why does the Federal Reserve aim for inflation of 2 percent over the longer run? Retrieved May 17, 2023, from

4 WorldData. (2022). Inflation rates in the United States of America. Retrieved May 17, 2023, from

5 BLS. TED: The Economics Daily (2022, July 18). Consumer prices up 9.1 percent over the year ended June 2022, largest increase in 40 years. Retrieved September 14, 2023, from

6 BLS. (2023, September 13). Consumer Price Index Summary. September 14, 2023, from

Мэ

An index is a portfolio of specific securities (such as the S&P 500, Dow Jones Industrial Average and Nasdaq composite), the performance of which is often used as a benchmark in judging the relative performance of certain asset classes. Indexes are unmanaged portfolios and investors cannot invest directly in an index.

Investing strategies, such as asset allocation, diversification or rebalancing, do not ensure or guarantee better performance and cannot eliminate the risk of investment losses. All investments have inherent risks, including loss of principal. There are no guarantees that a portfolio employing these or any other strategy will outperform a portfolio that does not engage in such strategies.

Past performance does not guarantee future results.